Buy to let property can be profitable, but you must be mindful of the taxes that you will have to pay, which will impact your revenue. Here is your definitive guide to tax on buy-to-let property, which details what taxes may be levied on your property, both when you buy it and also on the income you make from it.

Buy to let Stamp Duty

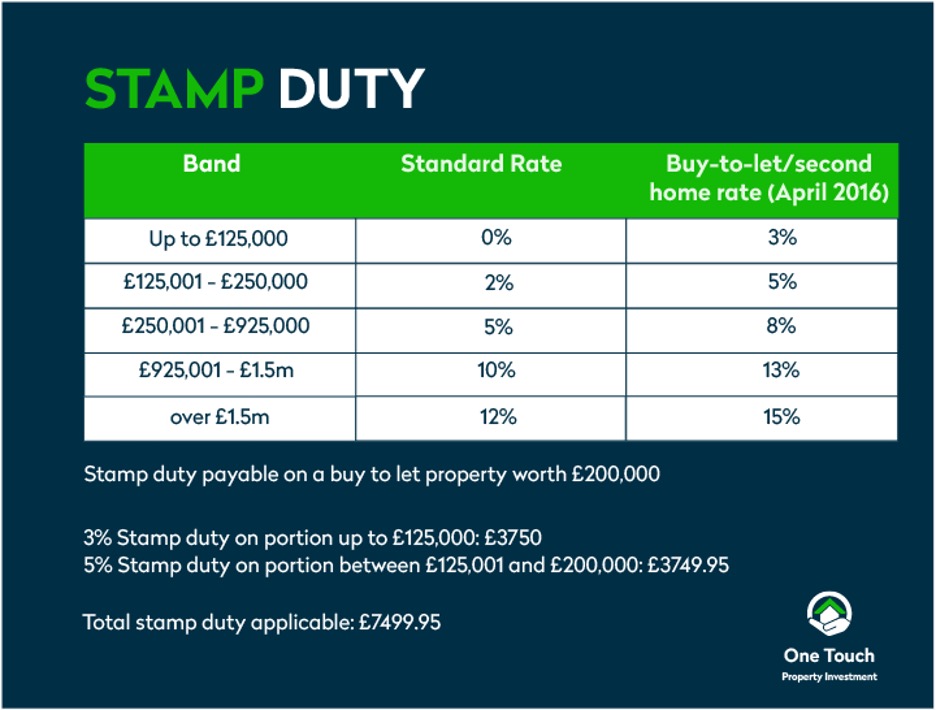

One of the first taxes you will pay on your buy to let property is stamp duty.

Stamp duty is applicable to anyone buying property over a certain price in England and Northern Ireland.

The current threshold is £125,000 for residential properties and £150,000 for non-residential land and properties. Any property bought below this value is not subject to stamp duty charges.

The tax is tiered depending on the value of the property. Below are the bands. It is worth noting if your property is £400,000, the entire sum is not subject to 5% stamp duty. 0% will apply to the first £125,000, 2% will apply to the portion between £125,001 – £250,000 and stamp duty will be applied at 5% to the portion between £250,001 – £400,000.

Stamp duty is applied differently to first time buyers and those buying a second property.

One can reduce buy to let stamp duty by purchasing student property or care homes rooms because it is commercial property and the stamp duty exempt under £150,000 purchase price.

One can reduce buy to let stamp duty by purchasing student property or care homes rooms because it is commercial property and the stamp duty exempt under £150,000 purchase price.

To explore the options in more detail you may benefit from learning more about the fundamentals of the student market and whether care homes are worth investing in.

It is worth noting that until March 2021 there is a stamp duty holiday. This means that only investors stamp duty is applied, and regular stamp duty rates are not applied.

From April 2021, those investing in UK property from overseas will be subject to an additional 2% stamp duty.

What is investor stamp duty?

Those looking to buy an additional property, either as a second home or as a buy to let, must pay an additional 3% stamp duty for each band as well as current rates.

Overseas investors, just like any investor, will pay stamp duty on property purchases. Most investors will have already purchased their own home, so an addition 3% of the total purchase price is to the usual stamp duty. It is otherwise known as second home stamp duty.

Married couples are considered one entity, so stamp duty would be applicable if either party purchased residential property. You cannot avoid investor second home stamp duty if your partner purchases the property in their name.

Up until March 2021, the government has introduced a stamp duty holiday, which means that only the additional 3% stamp duty is levied on property under £500,000 for investors. Other stamp duty rates are suspended.

Income tax on buy-to-let

Buy to let tax rules

There are a few changes to buy to let regulations and tax rules that you should be aware of before deciding to invest in the industry. The most notable being that landlords will no longer qualify for mortgage interest tax relief. Instead, landlords will receive a 20% tax credit for mortgage interest payments.

Capital Gains Tax is a tax applied to property owners who see their houses increase in value from the time they bought it to the time they sell it on. They are taxed on the increase with basic rate taxpayers taxed at 18% on the difference, and higher rate taxpayers taxed at 28% on the difference.

Before April 2020, if a landlord rents out a home that was once their main residence, Capital Gains Tax only applied to the amount the house went up in value when they were not living there. Before 2020, landlords could also add on an extra 18 months of time spent at the property, and this would also be exempt from Capital Gains Tax. From April 2020 this reduced to 9 months.

Mortgage interest tax relief

If you are wondering what mortgage interest tax relief is, you are not the only one. Prior to 2017, landlords could deduct mortgage interest payments from their profits before calculating tax. Since 2017 this has been gradually phased out and from the start of the 2020 tax year, landlords were no longer able to deduct mortgage interest payments from their rental income. Instead, you will only be allowed to subtract a flat rate of 20% of your mortgage expenses from your rental income.

Capital Gains Tax on buy to let

Capital gains tax on property can be avoided by purchasing commercial property under £150,000. Purchasing commercial property such as care home rooms and hotel room investments which provide a high yield is one way of reducing your capital gains tax obligation. Where properties are purchased on a long-term lease with contracted rate of return which is fixed, when it comes to selling the property the potential buyers would also want the same yield. So, where the yield stays the same, there is little chance of selling the property for a capital gain. That way capital gains tax is mitigated.

There are some ways you can lower certain taxes, such as buying property through a limited company. Although you may be subject to other corporation taxes. To find out more about buy to let taxes on investment property, read our full buy to let tax guide.